Mosaic Fertilizers opens vacancies for the Palmeirante (TO) Mixing Unit

In total, there are 18 job openings scheduled to begin in June this year; The project is still in progress

22.04.2024 | 15:56 (UTC -3)

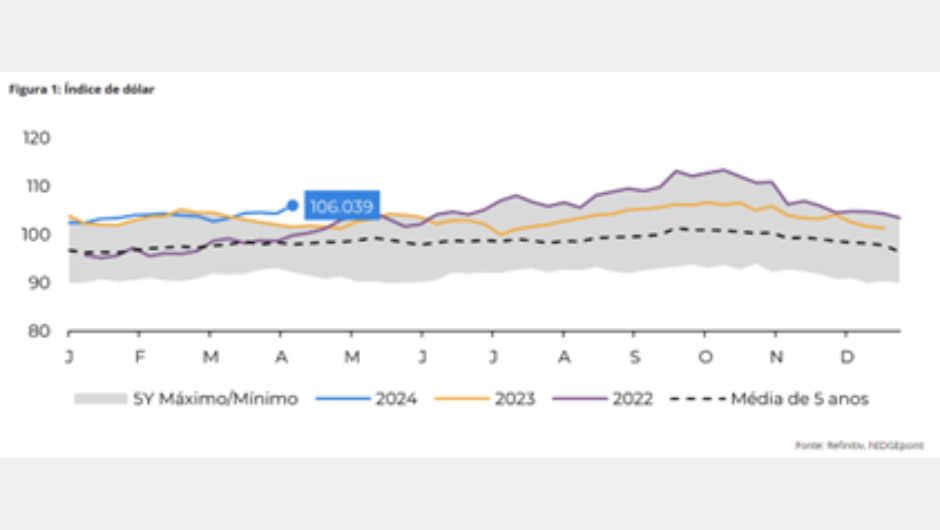

Last week started with a bearish macroeconomic environment. According to Lívea Coda, analyst at Hedgepoint Global Markets, the escalation of the conflict in the Middle East, combined with concerns about the results of the US IPC, increased the perception of risk in the market, aligning with the trend observed since the beginning of 2024.

“Improving U.S. Treasury yields could create more barriers for investors to add riskier assets to their portfolios. The idea that the Federal Reserve will postpone interest rate cuts has strengthened the dollar, creating a more challenging environment for commodity market participants, especially those where fundamentals are not strong enough, such as sugar,” explains the analyst.

“Another result of this bearish macroeconomic environment is the challenge that some emerging countries face. For example, the Brazilian Real suffered a devaluation of approximately 4% in April. This devaluation translates into higher returns for exports, helping to maintain a healthy export rhythm, even with some corrections in sugar prices”, he highlights.

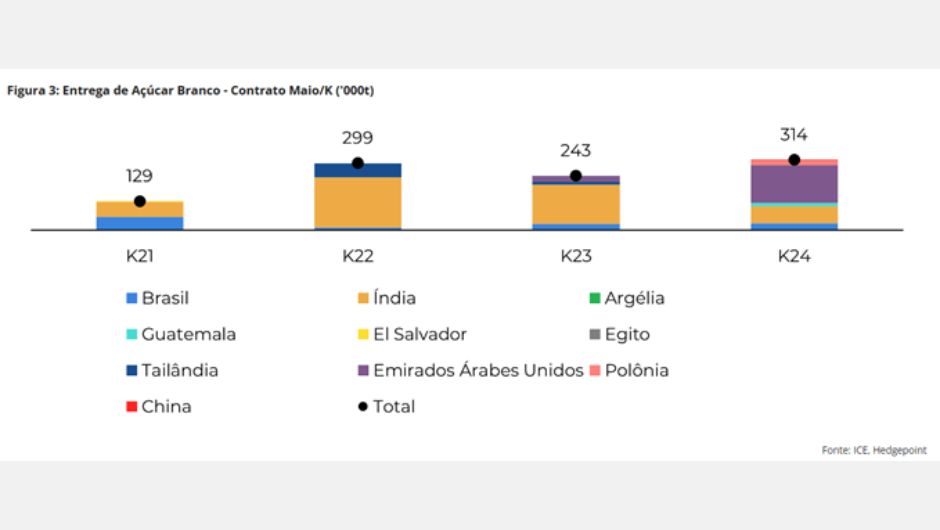

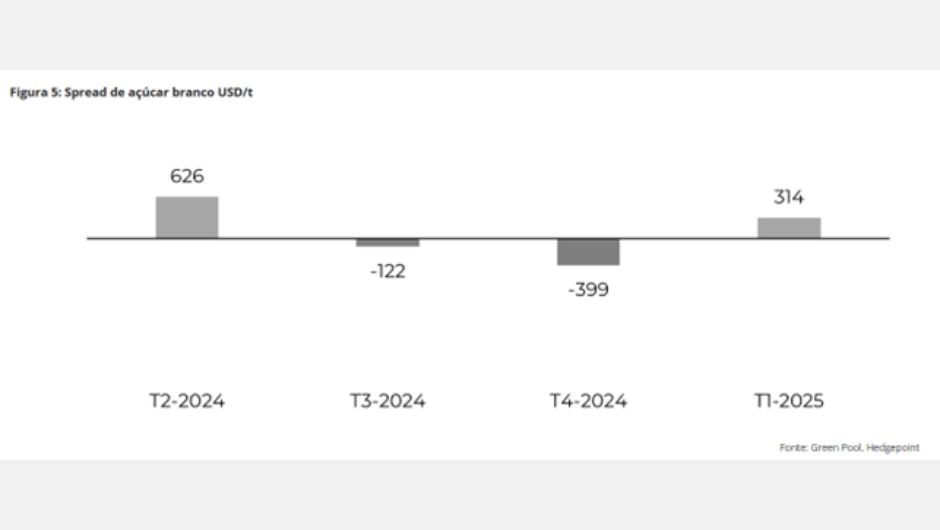

“In addition to the macroeconomic scenario, the week was marked by the expiration of the May contract for white sugar. Its final price was 615 USD/t, and the spread between the May and August contracts closed at an inverse of 35 USD/t. A total of 314kt of sugar was delivered, marking the highest level since at least 2021”, he comments.

“The majority of the volume was delivered by the United Arab Emirates, with significant contributions also from India and Brazil. Notably, this expiration was the first appearance in recent years of Poland and China among suppliers - a very intriguing participation”, he highlights.

Regarding Poland, the country's delivery could be a direct result of cheap Ukrainian sugar and the need to return some volume to the international market to support domestic prices.

“As discussed in previous reports, following the removal of tariffs on Ukrainian sugar by the European Commission, imports increased to over 400kt in 22/23 and are expected to increase further to 650kt in 23/24, reducing prices domestic sugar production in the EU”, he believes.

This increase in imports sparked protests across Europe, especially in France and Poland, by producers concerned about prices in the region. However, the EU extended its temporary free trade agreement with Ukraine until June 2025, with some safeguards.

“With the potentially greater influx of sugar imports and domestic price corrections, the region could increase its contribution to the global sugar supply, justifying its first appearance in recent years in an exchange delivery,” he says.

As for China, the country purchased raw sugar in December when prices allowed for import arbitrage in its non-producing states, estimated at 20,5c/lb. Consequently, Chinese customs recorded the highest volume of imports entering the country in January and February, which provided a floor for raw sugar prices in the market.

“With China’s harvest pace accelerating and considering its refining capacity, it is not surprising that traders are looking to capitalize on current white sugar prices, especially with fundamentals suggesting a possible correction ahead,” notes Lívea.

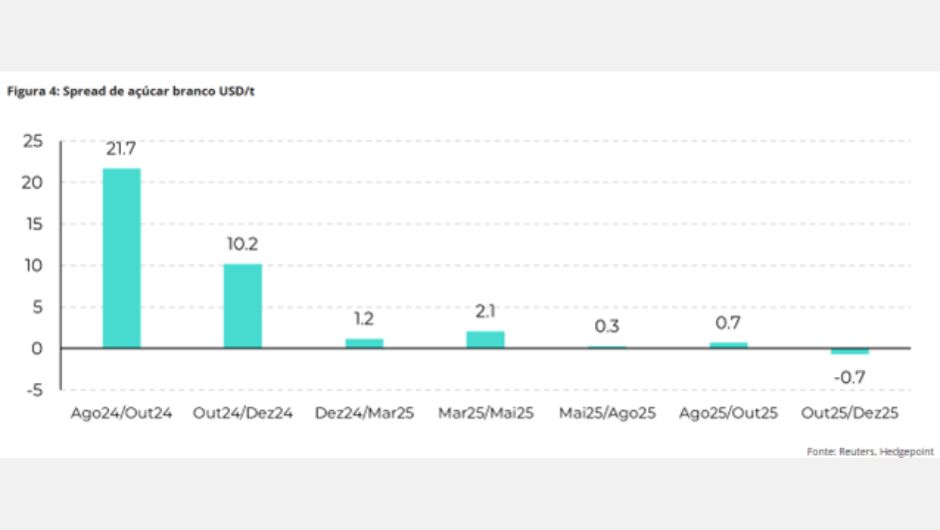

“Optimistic forecasts about sugar production in the Northern Hemisphere for the 24/25 season, a region known for supplying mainly whites, are reinforcing the current downward trend. The August contract failed to recover to levels prior to the May expiration and remains significantly lower than the 750 USD/t recorded at the end of 2023”, he analyzes.

The forecast of above-average monsoon conditions in India, together with favorable prospects for sugarcane development in other regions, contributes to the general expectation of greater sugar availability. The expected improvement is true even with the forecast reduction in the contribution of Brazil, one of the main producers of raw sugar. Given this bearish sentiment, supported by the sharp inversion in the white sugar curve, current prices could represent an opportunity for suppliers.

“Consequently, for the 2024/25 season, we forecast a modest surplus in the global sugar balance, estimated at around 500kt. This projection directly affects trade flows, especially in terms of white sugar,” he says.

It continues: “In contrast to previous years, when several important sugar-producing regions in the Northern Hemisphere suffered crop failures, white sugar trade flows are expected to remain relatively balanced for the remainder of 2024 and early 2025 , with a reduced surplus of approximately 400 kt”.

Last week began amid a bearish macroeconomic environment for commodities, driven by escalating conflicts in the Middle East and concerns about the US economy, increasing the market's perception of risk. The Fed's delay in interest rate cuts has strengthened the dollar, challenging commodities, especially those like sugar, with weak fundamentals. This environment also affected emerging countries, such as Brazil, which saw a 4% devaluation of the Real, increasing export returns, despite corrections in sugar prices.

The week was also marked by the expiration of the May contract for white sugar, which was set at US$615/t with a notable delivery of 314kt, mainly from the United Arab Emirates, India, Brazil and, surprisingly, Poland and China. China's past purchases of raw sugar and anticipated production increases signal potential market corrections. Optimistic forecasts for Northern Hemisphere sugar production in 2024/25 are reinforcing downward trends, with a modest projected surplus of 500kt.

Compared to previous years, the commercial flow of white sugar is estimated to be much more comfortable, which means that current prices could represent an opportunity for suppliers.

Receive the latest agriculture news by email

In total, there are 18 job openings scheduled to begin in June this year; The project is still in progress

With more than 420 thousand properties regularized in 2023, the State Government is campaigning to speed up the verification of another 260 thousand pending registrations