May: what will the weather be like in Brazil?

The forecast indicates above-average rain in much of the North and South regions

23.04.2024 | 15:17 (UTC -3)

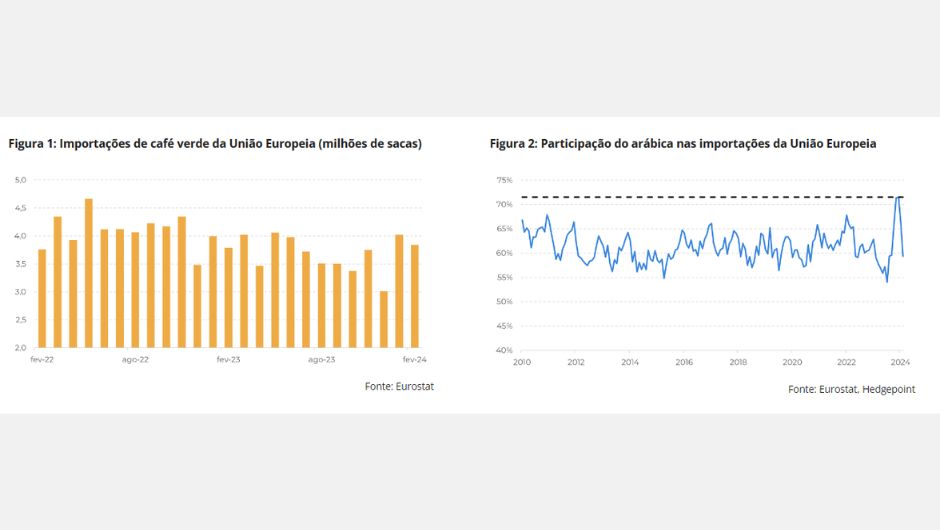

The European Union released import data for February - showing recovery, albeit limited. The bloc imported 3,84 million bags of green coffee, a drop of 5% compared to January.

According to Natália Gandolphi, Coffee analyst at Hedgepoint Global Markets, the movement is still well within the average (-9% between the two months, considering the historical series since 2010), which shows that, although the drop respected the seasonality, was much smoother than expected for the period.

“It is also important to note that the import profile is balancing after a strong swing towards arabica at the end of 2023. 60% of the imported volume was arabica, in line with the historical average (61%). The drop came after the bloc recorded the highest share of arabica imports since 2010 in December (72%).

The change reflects a balance after the pendulum swung so far towards the Arabica range, but also a clear concern about the volume of Robusta stocks in the bloc, with buyers preparing for a more intense squeeze on the Robusta market”, explains the analyst.

This could be for two main reasons: first, Vietnam will enter a seasonality of lower exports in the second quarter, and although the market is more dependent on other origins in Southeast Asia during this period, Indonesia may have another cycle of limited supply due to adverse weather during development and possible delays due to forecast higher levels of rain in the coming weeks.

In this scenario, it is already known that the bloc has been importing more coffee from alternative origins, including from Brazil. In March, this volume reached a record: 2,18 million bags of arabica and conilon (the previous record in the short-term series was recorded in November 2020).

“Now, with the next harvest of the 24/25 cycle in Brazil, the market expects volumes to alleviate part of the deficit, especially from July onwards. Fixings for the 23/24 cycle advanced in the last quarter, with 96% of the conilon harvest already sold in April. With a production of 22,54 million bags, this would represent less than 1 million bags in net stocks (stocks that have only been sold, and not necessarily exported or consumed domestically; as a general rule, gross stocks are generally 3 to 4 times greater than liquid stocks, but it is known that this varies greatly between harvests)”, he observes.

In this scenario, the 24/25 harvest already consolidates its leading role, and sellers must act in accordance with the daily changes in climate forecasts observed for the main Robusta producer, Vietnam.

“Soil moisture levels are considerably low, but the forecast has recently changed to suggest the dry period may be coming to an end. By observing the development of the situation in Vietnam, the market will be able to observe points of sales pressure”, he believes.

February import data from the European Union shows some recovery, with 3,84 million bags of green coffee imported, 5% less than in January, but within historical seasonal patterns. The import profile rebalanced to 60% Arabica, reflecting concerns about Robusta stock volumes and the further contraction of the Robusta market.

Supply challenges in Vietnam and Indonesia could also further hamper the availability of Robusta in the 24/25 cycle. The EU increased imports from alternative origins, including from Brazil, reaching a record in March. As Brazil's 24/25 harvest approaches, the market expects an alleviation of the deficit shortage from July onwards, but in the meantime, the market will closely watch the changing weather pattern in Vietnam.

Receive the latest agriculture news by email

The forecast indicates above-average rain in much of the North and South regions

The event took place from April 5th to 14th and brought together more than five thousand animals, as well as the main national manufacturers of agricultural machinery and vehicle dealerships.